Infrastructure Protects Production.

Independent anti-money laundering ("AML") reviews and executive compliance oversight for mortgage brokers who don’t want licensing delays, lender issues, or regulatory surprises.

Compliance infrastructure for serious mortgage brokers navigating AML reviews, regulatory oversight, and long-term operational stability.

If Any of These Sound Familiar…

- Your AML review is overdue.

- A lender requested compliance documentation.

- Your renewal is approaching.

- You are not sure whether your AML program would survive an examination.

- You assumed someone else was handling it.

You may realize you need infrastructure.

Most mortgage brokers aren’t negligent. They were never taught what regulators actually expect.

Mortgage brokers are wired for production.

Pipelines. Rates. Realtor relationships. Closings.

Compliance requirements — including independent AML reviews and state examination standards — often live in the background until a regulator notice arrives.

The issue isn’t irresponsibility. It’s assumption.

Compliance infrastructure replaces assumption with operational clarity.

Compliance is Infrastructure.

Mortgage compliance is often treated as a regulatory obligation.

Serious broker-owners treat it as business infrastructure.

Infrastructure protects:

- License renewal and regulatory standing

- Lender approvals and correspondent relationships

- State examination outcomes

- Production continuity during market volatility

- Long-term enterprise value

If you are building a serious mortgage brokerage, compliance infrastructure is not optional.

What Happens During an AML Review

Initial Compliance Assessment

Documentation Review

Gap Identification

Independent Review Report

Recommendations

Exam Readiness Guidance

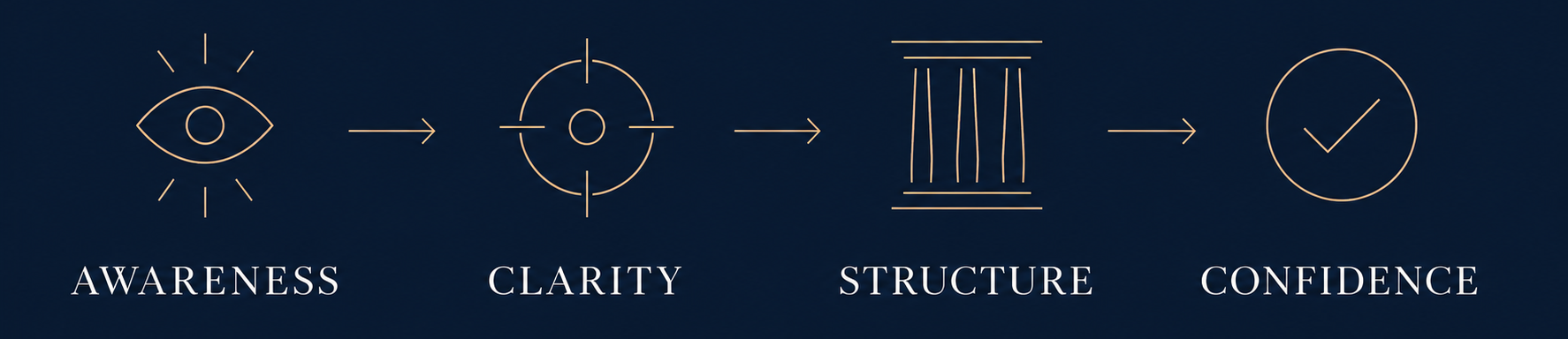

The ACS Compliance Method

An executive framework for AML compliance and regulatory preparedness for independent mortgage brokers.

Awareness

Identify blind spots in your AML program and regulatory exposure before they become urgent.

Clarity

Translate federal and state mortgage compliance requirements into plain English.

Structure

Operationalize your AML policy, documentation standards, and internal oversight processes so they withstand examination scrutiny.

Confidence

Move from “I think we’re compliant” to “We are prepared for our next independent AML review and state exam.”

Compliance only protects your mortgage business when it is understood, implemented, and independently reviewed.

Independent Oversight. Executive-Level Compliance Advisory.

AML Independent Reviews for Mortgage Brokers

Independent AML reviews aligned with FinCEN guidance and state regulatory expectations — structured to protect license renewal and lender relationships.

Mortgage Examination Readiness & Executive Regulatory Advisory

Preparation for state examinations, regulator inquiries, lender approval reviews, and compliance program documentation audits.

Executive Compliance Advisory for Broker-Owners

A capped executive advisory relationship focused on infrastructure maturity, AML program oversight, and long-term regulatory risk containment. Enrollment opens twice annually. Consultation required.

Compliance Subscriptions Do Not Equal Compliance Protection.

Many mortgage compliance vendors provide policy templates, portals, and bundled services.

Templates do not create compliance.

An AML policy that is not customized, monitored, and operationalized does not protect your brokerage during a regulator exam.

Protection requires independent review, implementation oversight, and infrastructure discipline.

Producers Focus on Revenue.

Executive Operators Protect Infrastructure.

Mortgage brokers who operate at an executive level:

- Verify AML program oversight.

- Schedule independent AML reviews proactively.

- Align compliance policies with operational reality.

- Prepare for regulatory exams before they are announced.

Infrastructure is the difference between reactive compliance and executive-level regulatory protection.

This Practice Is Designed For Mortgage Brokers Who:

- Plan to remain in the industry long-term

- Value infrastructure over reactive compliance

- Care about lender approval stability

- Want clarity around AML requirements and regulatory expectations

- Prefer independent executive oversight over bundled subscription services

Not every broker is the right fit.

Build Compliance Infrastructure Before It Becomes Urgent.

If your independent AML review is approaching, your license renewal is pending, or you want executive-level clarity around mortgage regulatory compliance, schedule a confidential conversation.

Schedule a Conversation